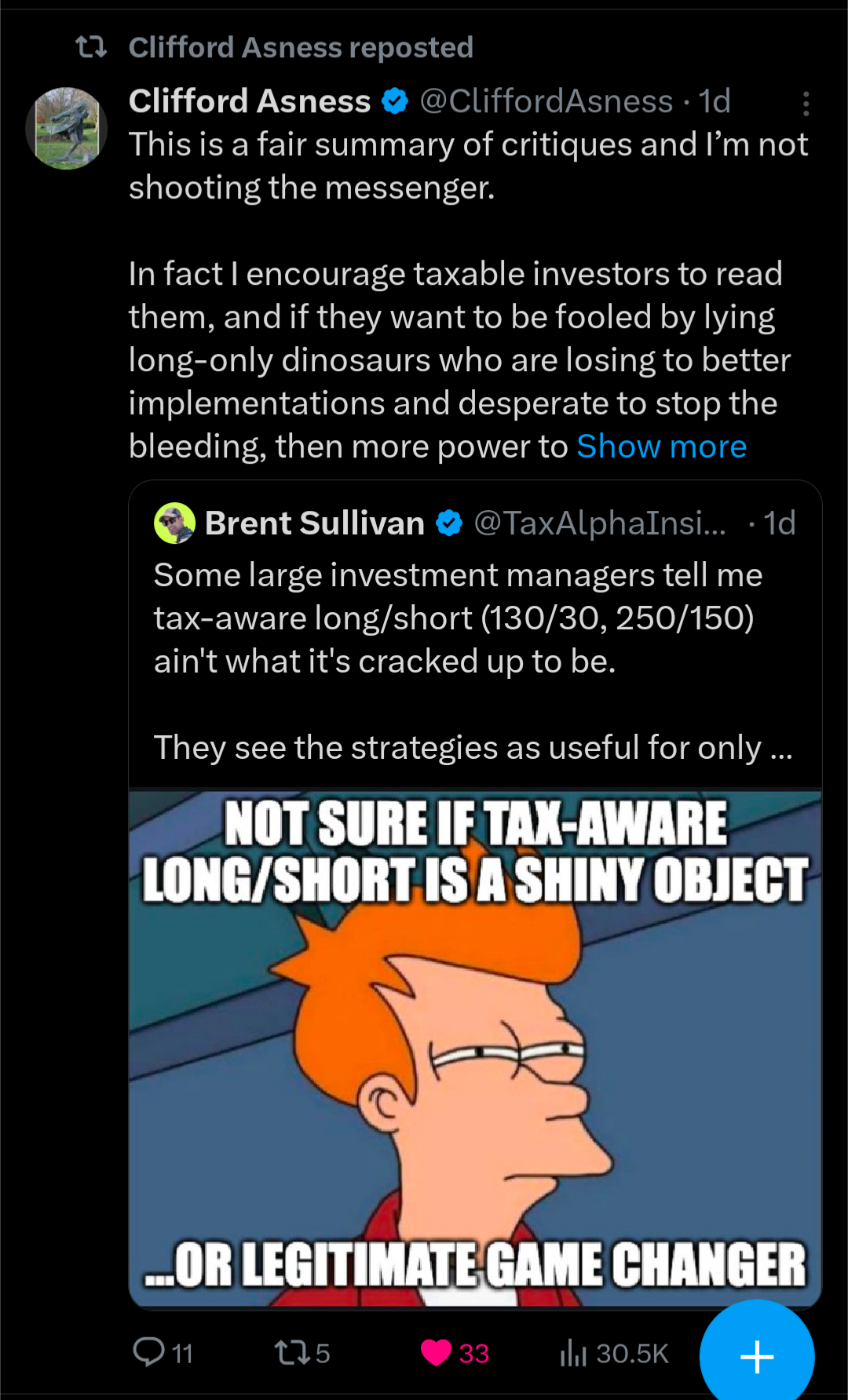

Cliff Asness: "...lying long-only dinosaurs... desperate to stop the bleeding..."

Ignore tax-aware long/short at your peril

That's Cliff Asness ripping into the tax-aware long/short naysayers, whose critiques I listed in a recent post.

My reaction is 🍿🍿🍿… until I remember that I kicked off this “debate” (it’s not a debate) and feel responsible for ushering it forward.

So, I’m pleased to say that some serious investors and advisers have agreed to go on the record to address the critiques point-by-point, so stay tuned.

To be clear, tax-aware long/short is the most exciting development in taxable investing in decades.

I’ve written about it countless times:

Direct indexing can't keep up with the net capital losses a tax-aware long-short

There are several more… but you get the point

In fact, I’ve been writing about tax-aware long/short since the summer of ‘22 when I stumbled on Andrew Berkin’s Having Your Cake and Eating it Too, and then on Constantinides’ papers from the early 1980s, before finally going down the AQR rabbit hole and binging their papers.

I’m fully bought in.

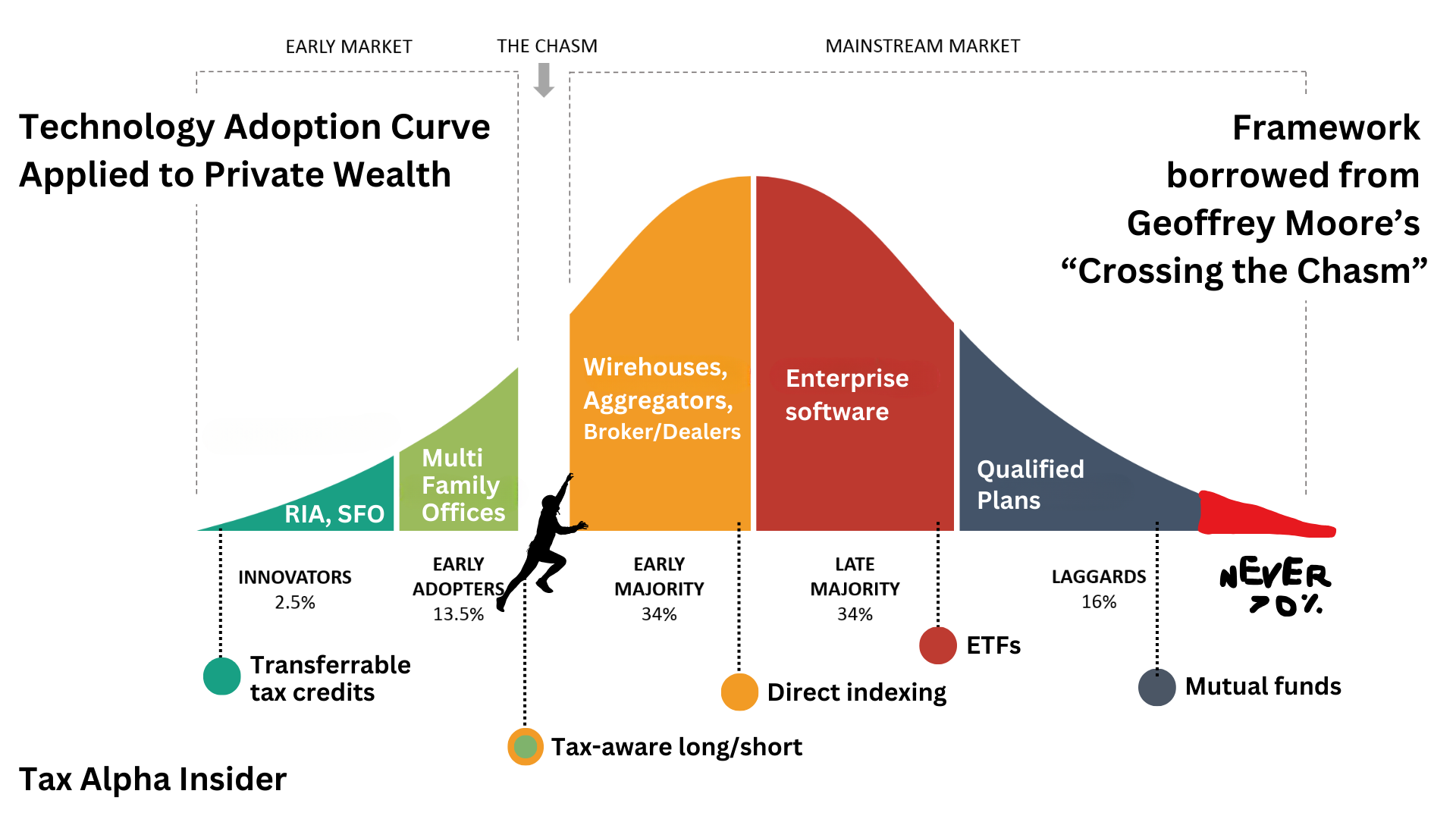

My instinct is that tax-aware long/short is crossing the chasm

In other words, it’s gonna go mainstream if it’s not already there.

Btw, here’s an AUM update, which may warrant monthly revisions b/c this darn thing is growing so fast:

AQR: Tax-aware long/short AUM ~$13.2 billion (12/31/2024)

Quantinno: Tax-aware long/short AUM ~$13 billion (source familiar)

BlackRock/Aperio: Tax-aware long/short AUM ~$1 billion

There are more players (Parametric, Brooklyn, Gotham, etc.), but I don’t have any hard figures.

Every time I write about tax-aware long/short, I get pushback

So, let’s put the pushback in context. Here is how I see the universe of builders/vendors and buyers/advisers of tax-aware long/short:

Buyers (i.e., advisers):

Ecstatic: Tax-aware long/short is the shit. It changes everything, helps them win business, and deliver better results for their clients.

Yawn: They need to get comfortable with leverage and shorts, or they don’t care to understand the risks (or how they’re managed), or tax-aware long/short isn’t a fit for their clients (too small, too distracted, etc.).

Oblivious: Still haven’t heard of tax-aware long/short. Or the infamous “you’re losing money to save money?!” challenge that is hard to recover from but very common.

Builders (i.e., vendors, sub-advisers, competitors)

Committed: Tax-aware long/short is the hook that wins business and is a significant product and distribution effort.

Queued up: Will eventually build or partner, but it’s not top priority.

Dismissive: Tax-aware long/short is a distraction. How big can it really get? They can’t win in that category, so they stay in their lane.

Competitive: Tax-aware long/short is actively harmful. Look at all the ways it can go wrong. Look at how hard it is to explain, etc.

If these bullets remind you of anything, it might be the technology adoption curve I showed above. We have the early adopters/innovators (the ecstatic advisers, the committed vendors), the folks who need more convincing (the “yawn” advisers and the “queued up” vendors), and finally the holdouts/laggards (the “oblivious” advisers and the “dimissive/competitive” builders).

This was supposed to be a short note, so let me wrap it up with a red herring.

Why are we talking about full liquidation and short-term capital gains?

Some of the doubt in tax-aware long/short is unfounded. It’s subtle, though, so let’s talk about it.

BlackRock’s paper on tax-aware long/short is thoughtful and interesting and says the following:

Liquidation reduces TA [tax alpha] by about half, while a lack of short-term capital gains to offset reduces TA by approximately 40%. In combination, those investor characteristics may render a long-only loss harvesting portfolio or a low-cost ETF more desirable than a long/short tax-managed equity portfolio after costs and fees are taken into consideration. [emphasis mine]

This little quote from the abstract has given a few allocators reason to dismiss or attack tax-aware long/short.

Here’s a quick summary and rebuttal (narrative, not real quotes):

Critique: "See, liquidation makes tax-aware long/short dumb.”

Response: “How often do investors fully liquidate? Not often. That’s sorta the point of the tax management.”

Quick aside:

The BlackRock/Aperio team explain why they chose to study pre- and post-liquidation scenarios, acknowleding that a bequeathing scenario isn’t as draconian:

“Pre‑ and post‑liquidation The tax treatment of a portfolio at the end of the investment horizon varies with investment vehicle and investor disposition. For example, in an estate event, a long-only portfolio held in a separately managed account may be transferred to an heir. In this case, cost basis can be reset to contemporaneous market price—eliminating a potentially signifcant tax liability. The end-of-horizon treatment of a long/short portfolio is more complicated because short positions may not be bequeathed. Some investors liquidate their portfolios, in which case tax must be paid on capital gains. Since the benefts of tax management depend materially on what happens at horizon end, we include both pre- and post-liquidation analyses in our study.”

Critique: “Well, what if investors don’t have short-term gains needing offset. THEN tax-aware long/short is overkill.”

Response: “Most really tax-inefficient products usually go in tax-advantaged/exempt accounts (that’s basic asset location), so it makes sense there aren’t many short-term capital gains needing offsetting. But short-term capital gains, however rare, are just one problem that tax-aware long/short solves. The other problems it solves are:

reanimating ossified portfolios 💀

diversifying single-stock positions

banking losses BEFORE business or investment property exit

smoothing capital gains spikes AFTER business or investment property exit

wrapping tax-inefficient products (e.g. mutual funds) for a tax-neutral exit

more (and more persistent) tax-losses for use during an investor’s consumption phase (even if gains are long-term)

providing more low-basis options for future charitable giving

etc. The list goes on…

And I’m just talking about tax here. There are pretax arguments that are outside my expertise but should be the motivating factor for any investment, while this tax business, honestly, is an optimization.

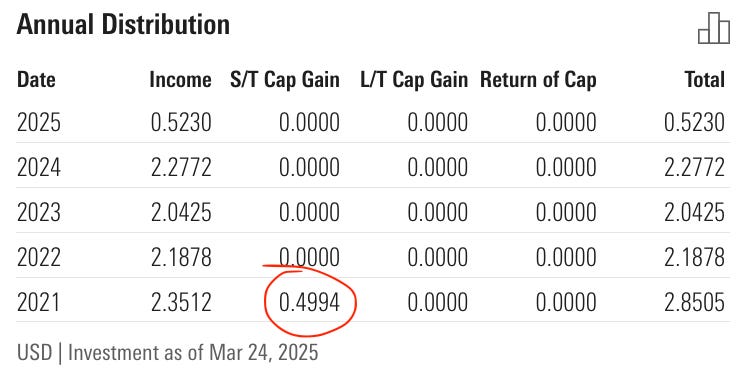

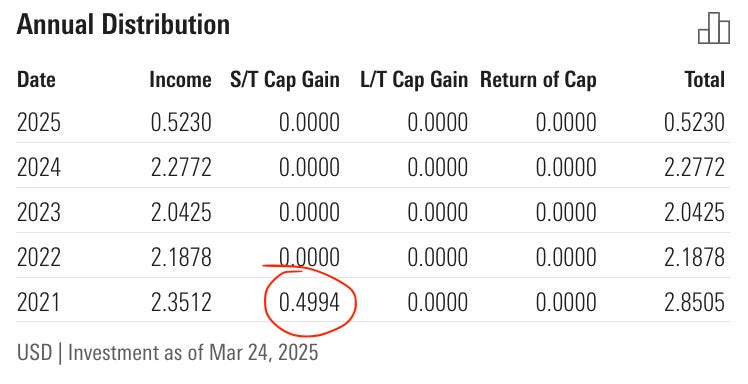

Finally, short-term gains are acute (especially in CA and other highly-taxed states, advisers always emphasize to me). I’ll just quickly mention that some ETFs (and other products, undoubtedly) produce short-term gains unexpectedly. Hence, it’s wise to have short-term losses banked.

Surprise! Source: Global X NASDAQ 100 Covered Call ETF QYLD

Another quick aside:

I list a bunch of cool use cases above (directly from advisers) that could be interesting to quantify at some point.

One final thought is that by using liquidation and lack-of short-term capital gains as essentially stress tests that tax-aware long/short must pass, which it does in nearly all cases, the BlackRock/Aperio authors have established a lower bound that less punishing cases will almost obviously trip over. In other words, tax-aware long/short passed the hard test (mostly) and passing easier tests will be, uh, easier.

This was supposed to be a fast follow-up to Wednesday’s post

…but I’ve written a short book. Sorry.

And yet, there’s still much more to cover following my interviews scheduled for next week with the investors and advisers who want to address the original critiques (which include cost, negative pretax alpha, tracking error, long/short incremental risk, and more).

There’s plenty more to unpack. Stay tuned…